TLDR; Allogeneic cell therapies are here to stay, just fewer of them with a clearer value-add.

Fate Therapeutics began 2023 with a whimper.

Once a darling of the allogeneic cell therapy surge in recent years, in January Fate announced it was laying off more than half its workforce, terminating a key collaboration with Janssen and cleansing its pipeline of most of its NK and T cell based therapies. Once worth $10Bn, the company’s rapid shift in fortune following underwhelming data has cast serious doubt over the future of allogeneic cell therapies.

Big pharma players are beginning to voice their scepticism.

Christi Shaw, CEO of Kite, on a media call alongside Gilead’s earnings in February admitted it would be “quite a while, if ever” before off-the-shelf cell therapies caught up with autologous offerings. Gilead’s recent deals with Arcellx and Tmunity (another zero-to-hero-to-zero cell therapy biotech of the recent years) were both positioned as reinforcements for their autologous offering.

Novartis has opted to invest in rapid manufacturing for their autologous CAR-T cell therapies, sending a not-so-subtle message that they see the immediate future in enhancing the current (albeit complex) supply chain. However, despite whittling down manufacturing times to just two days, capacity limitations mean there is still a way to go in solving cell therapy’s biggest bottleneck.

Elsewhere, other big pharma players including Roche, Pfizer and Sanofi are all keeping a sizable toe in the water to see if allogeneic therapies can deliver on the many promises.

However, pessimism surrounding off-the-shelf therapies may be premature.

In December 2022 Atara Biotherapeutics secured a CHMP recommendation for Ebvallo for patients with post-transplant lymphoproliferative disease who are positive for Epstein-Barr virus, meaning Ebvallo is now poised to become the first allogeneic T-cell therapy approved in the world. Atara is still reeling after Bayer pulled out of a $670 million partnership on their autologous therapy earlier that year, but the anticipated approval of Ebvallo marks significant milestone for the industry, with additional clinical trials ongoing.

Similarly, Beam Therapeutics got the go-ahead from the FDA to continue with human testing for a base-edited, off-the-shelf CAR-T therapy in a certain type of leukemia.

It is not autologous ‘versus’ allogeneic, there is need for both approaches to co-exist.

Given that autologous ‘versus’ allogeneic is a convenient narrative used by investors and developers, which often align only with one side of the aisle, it is easy to lose perspective and nuance. There is a popular notion that allogeneic will ‘cannibalise’ the autologous market share. This may be partly true in some cases, but downplays the complementary advantages of access to both these approaches.

Fundamentally, allogeneic cell therapies are still in their infancy both clinically and commercially. Safety, efficacy, and durability of these therapies largely remains to be proven. As time goes on, the specific use cases for allogeneic approaches in the clinic are only becoming clearer.

Let’s consider several timely potential use cases for off-the-shelf therapies:

- Autologous cell therapy is unsuccessful

Although the manufacturing success rate of CAR-Ts on the market is approaching 95%, there remains a critical subset of patients where allogeneic therapy will provide a potential lifeline. With well over 3000 patients now treated with CAR-Ts, there is a growing portion of the population where autologous cell therapy is not a viable option for a host of logistical and clinical reasons.

One key subset it those patients who relapse after autologous CAR-T cell therapy. It is not yet clear how best to treat these patients in lymphoma, but allogeneic approaches are considered among the best options in development. Leading US physicians Caron Jacobson (Dana-Farber Cancer Institute) and Frederick Locke (Moffit Cancer Centre) have both recently highlighted the need for clearer options for patient who relapse after an autologous CAR-T cell therapy.

- Quality cells are not available

The quality of the starting material is paramount for autologous cell therapy. In certain cases, patients have already undergone multiple rounds of chemotherapy and may be fragile. In these instances where high-quality cells cannot be obtained, allogeneic provides an alternative route for the most at-risk or urgent cases.

- The current autologous supply chain is too restrictive

Although now over 300 centres across the world can deliver autologous CAR-T cell therapy, the infrastructure for the care continuum is already getting strained despite relatively low numbers of patients treated and products on the market. Bottlenecks have emerged at multiple points of the autologous supply chain, leading to an ongoing game of logistical ‘whack-a-mole’ to tackle limitations in manufacturing capacity, turnaround, scheduling and hospital capacity. Furthermore, global and emerging markets remain largely untouched by CAR-T cell therapy.

Current approvals and pipelines have also stayed within a narrow slice of the disease spectrum, namely haematology. The emergence of cell therapies to treat new disease areas in immunology, cardiology and neurology will demand higher patient volumes and repeat dosing, greatly favouring the relative logistic simplicity of off-the-shelf therapies.

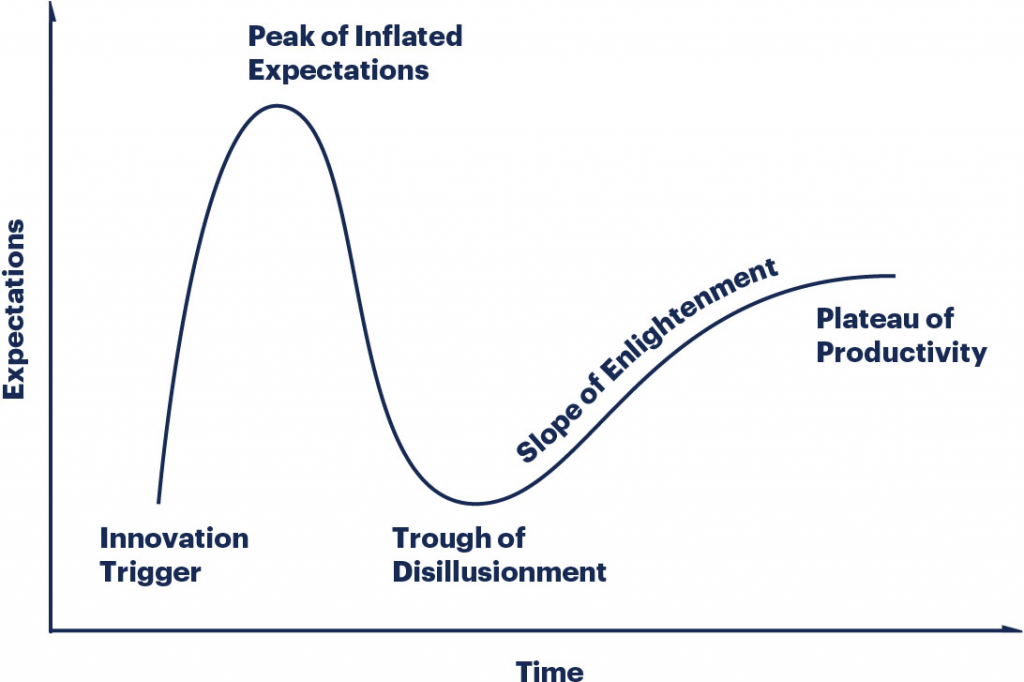

Looking ahead … riding the hype curve.

Tales such as Fate Therapeutics are not the death of a new industry or technology platform, they are its first true reality check.

This moment is the familiar plunge of the technology hype curve, when the peak of inflated expectations (and company valuations) leads to disillusionment and consolidation which eventually paves the way for productive and sustainable progress.

Allogeneic will not be last to face this ride either. Additional approaches are also in development.

Manufacturing autologous cell therapies at the point-of-care (POC) is gaining speed, championed by companies such as Miltenyi Biotech, Lonza, SQZ Biotech, Orgenesis and Ori Biotech. Alternatively, in vivo generation of CAR cells could eliminate the need for gene editing of immune cells outside the body altogether. This approach also has its challenges, but offers the potential to combine some of the benefits of both autologous and allogeneic cell therapies.

It is only a matter of time before allogeneic developers solve the durability challenge.

Allogeneic developers should take inspiration from the success of autologous therapies, and the pace at which scientific challenges have been overcome. For context, the first autologous CAR built to target CD19 was developed in 2003 and it would be 14 years before Kymriah was finally approved. Comparatively, the allogeneic cell therapies have only undergone significant clinical testing since 2020.

Furthermore, despite graft versus host disease (GVHD) being a major stumbling block for early allogeneic therapies, after the discovery of the major role TRAC KO plays in preventing GVHD there has been no GVHD cases reported in recent data releases at ASH 2022.

More failures please.

Tales such as Fate Therapeutics should not deter the development of allogeneic therapies. On the contrary, they should be seen as the signs of a hard-fought learnings which must accompany a frightening pace of innovation.