Introduction

MFN pricing pressures are compressing margins and challenging the economic viability of Western pharma manufacturing in Europe, particularly for innovative and high-cost therapies. Indeed, MFN pricing functions both as a direct pricing constraint and as a strategic signal, accelerating portfolio prioritization, geographic rebalancing, and supply chain reassessment.

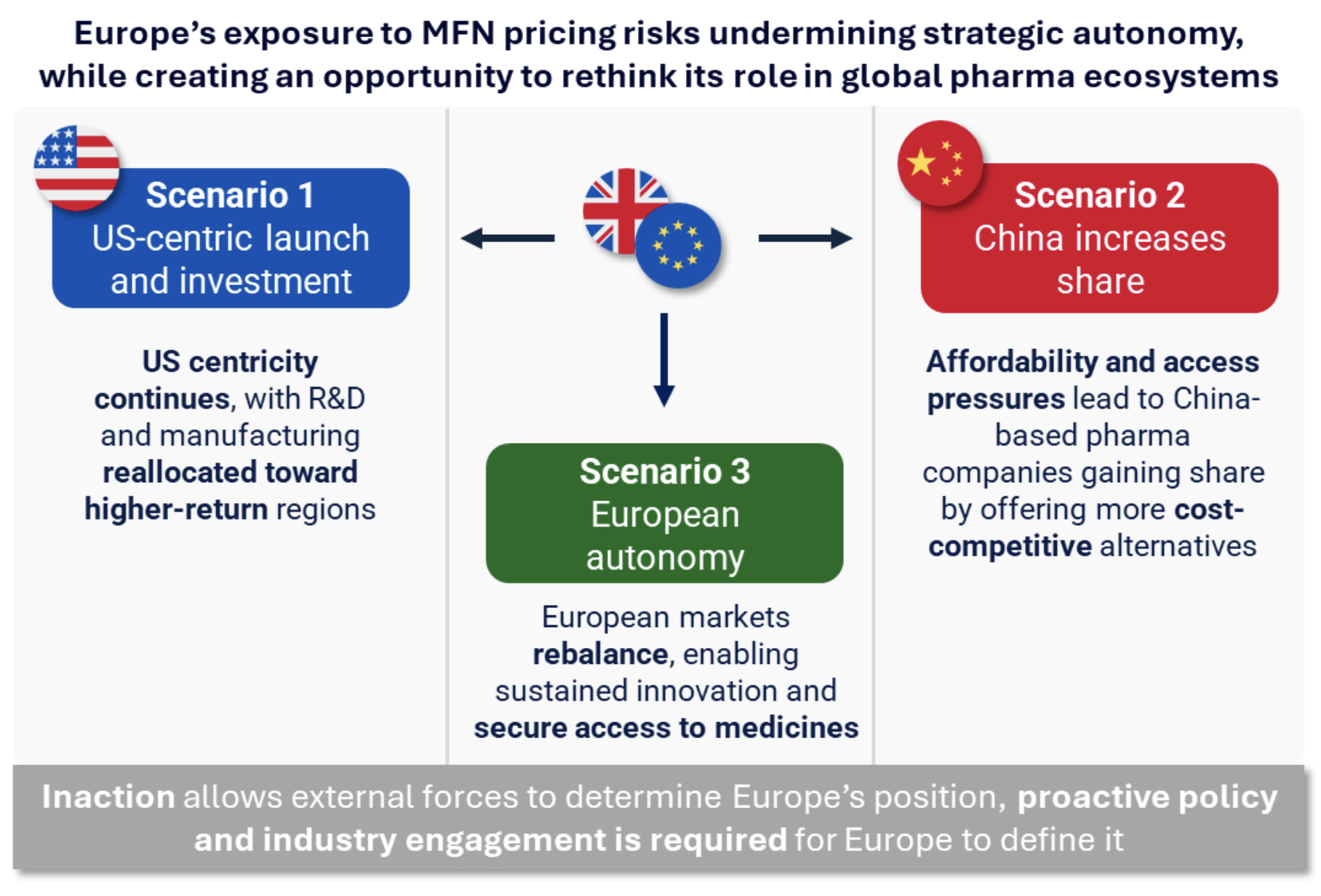

Europe is particularly exposed to MFN pricing as it operates within a cost-sensitive, access-driven pricing environment with high regulatory complexity and fragmented reimbursement systems which can weaken relative incentives for local investment and manufacturing. However, this exposure creates a catalyst to rethink Europe’s role in the global pharma ecosystem, driven by three competing directional forces:

- Continued US-centricity of global pharma investment and launch sequencing

- China-based manufacturers claim an increasing share of EU market

- A policy-driven rebalancing toward greater European autonomy.

In this white paper, we explore scenarios based on the potential outcomes of these competing forces and examine how European markets can adapt to MFN realities to maintain their position as a globally leading market.

Scenario 1: Global investment and launch priorities increasingly concentrate in the US, with Europe receiving reduced focus across R&D, manufacturing, and access

Scenario 1: Global investment and launch priorities increasingly concentrate in the US, with Europe receiving reduced focus across R&D, manufacturing, and access

In this first scenario, companies sustain the current US-led global strategies, with launch sequencing, pricing, and capital allocation being anchored to the US market whilst limiting investment in Europe. For example, R&D and manufacturing footprints would be selectively reallocated toward higher-return or policy-supported regions, with parts of Europe deprioritized over time. Europe would effectively become a secondary priority in global allocation decisions, with implications for slower access to innovative medicines and reduced negotiating leverage.

Furthermore, governments would face persistent challenges in securing timely supply and access, driven by launch delays, selective market entry, and added complexity from the structural disconnect between centralized regulatory approval and fragmented national pricing and reimbursement systems. Indeed, while mechanisms such as the Joint Clinical Assessment (JCA) centralizes evidence review and has been successful in decreasing regulatory review timelines (Ojemda was approved in 10 days compared to the 30-day timeline specified under EU HTA regulation), the JCA leaves pricing and access decisions at the national level.

Scenario 2: Affordability and access pressures drive greater reliance on China-based manufacturers and partnerships to supply the European market

Both continued and increasing US-centricity in global pharma leaves gaps in European access and affordability, which creates openings for China-based players to expand presence in the EU market. In this scenario, China-based pharma companies, either directly or through partnerships, gain market share by offering more cost-competitive alternatives. While China is established in providing active pharmaceutical ingredients (APIs), there is evidence of developed capabilities and a gradual shift beyond APIs toward developing branded and innovative products which could begin to compete in European markets.

However, execution of high-cost therapies at scale remains to be proven and geopolitical and regulatory factors may act as both accelerators and constraints. For example, increasing scrutiny of foreign ownership, data, supply chain resilience, and regulatory standards could slow integration of Chinese products into Europe even as economic pressure encourage selective collaboration.

Despite ongoing uncertainty, early signs of engagement with China are emerging, with European stakeholders such as British Prime Minister Kier Starmer, who visited China in January 2026 to discuss trade and investments, and companies such as AstraZeneca, which announced a $15B investment in China through 2030 to expand medicines manufacturing and R&D, indicating a potential diversification of partnerships beyond the US. Indeed, China’s pharmaceutical sector is actively seeking to commercialize its growing pipeline in global markets, with Asian out-licensing deals constituting ~25% of the global total in 2024, and those originating in China generating $800M in upfront payments in 2024, up from under $100m in 2020. European multinationals are increasingly serving as the acquirors of these rights, illustrated by AstraZeneca, Novartis, Merck KGaA and Sanofi all structuring major licensing deals with Chinese companies in 2025. With limited domestic reimbursement constraining Chinese market returns, and the US presenting growing geopolitical friction, the EU represents a natural expansion target.

Over time, Europe risks increasing strategic dependency, with reduced influence over innovation pathways, supply chain resilience, and a long-term manufacturing base.

Scenario 3: Through coordinated policy and industry action, European markets rebalance and strengthen strategic autonomy, enabling sustained innovation and secure access to medicines

Differences in healthcare system design have historically underpinned pricing variation, with the US rewarding innovation through higher prices and rapid uptake, Europe prioritising affordability and access through tighter price controls, and China operating at structurally lower cost levels. While Europe sits between US and China pricing models, it needs to move closer to the centre of global benchmarks to counter Scenarios 1 and 2 and remain competitive.

Indeed, to strengthen Europe’s strategic autonomy, European stakeholders should align to reinforce the value of healthcare innovation and the strategic importance of maintaining a strong regional pharma base. Similarly to how defence spending has been anchored across European markets to a defined share of GDP to ensure stability and independence, allocating a percentage of GDP to innovative medicines could provide a coordinated and sustainable foundation to support investment, access, and long-term healthcare resilience. The concept is gaining traction, for example Pfizer’s CEO invoked the NATO spending analogy at the Goldman Sachs Healthcare Conference in June 2025, noting that the U.S. spends ~0.8% of GDP on innovative medicines compared to 0.3% in the UK, 0.4% in Germany, and 0.5% in Italy and Spain. Since then, the UK committed to doubling spending on innovative medicines as a proportion of GDP, from 0.3% to 0.6% over the next 10 years, as part of the deal to secure 0% tariffs on pharmaceutical exports to the US.

More specifically, pharma companies and industry bodies should increase coordinated advocacy, linking investment in Europe to broader outcomes such as health system sustainability, economic contribution, and productivity gains. Additionally, local manufacturing, R&D, and innovation should be actively incentivised through targeted national and EU-level policies (e.g. funding mechanisms, regulatory flexibility, and common industrial strategy).

If successful, coordinated EU and Member State policy frameworks would emerge, reducing fragmentation and enabling more predictable access and investment environments. Then, pricing and access systems could evolve to better reward innovation and speed of access, potentially including modest increases in net price levels, as seen in the UK’s commitment to increase the net price paid on new medicines by 25%, or improved commercial conditions to sustain investment.

Illustrative signals of a successful onshoring of pharma capabilities could include expanded public-private partnerships, faster adoption pathways, and companies increasing European footprint commitments in exchange for improved access conditions. Long term, Europe would have strengthened its position as a self-sustaining innovation and manufacturing hub, with reduced external dependency and improved access to innovative medicines.

Conclusions

Europe and biopharma have a window to rebalance their relationship and enable a more predictable, mutually beneficial, and sustainable investment in healthcare and innovation. In the absence of coordinated action, Europe risks defaulting to Scenarios 1 or 2 and would cede control over investment, access and supply dynamics. Proactive policy and industry engagement is required to shape and realize Scenario 3, and develop a more resilient, innovation-driven, and strategically autonomous European healthcare ecosystem.