What is likely the overall impact of the reduced free pricing period for pharma launch strategies in Germany, the EU, and the world?

Introduction

Increasing healthcare burden in Germany and the world necessitates economic reform

Germany has been a top priority market for launch in the EU, establishing it as a market known for rapid patient access to novel medicines, especially after the AMNOG law of 2011. However, recent news of the “Statutory Health Insurance (SHI) Financial Stabilization Bill” (GKV Finanzstabilisierungsgesetz) which will shorten the free pricing period to 6 months from 12 months(1), has cast a shadow of doubt over the future of this status. The changes to the German HTA process are expected to offset rising healthcare costs and lay the groundwork for a more sustainable system but are also anticipated to come at a major cost to manufacturers and potentially even patients. Looking forward, the impacts of the reduced free pricing period are likely to have ripple effect for pharmaceutical launch strategies in Germany, across Europe and beyond.

The “Statutory Health Insurance System Financial Stabilization” Law (GKV-Finanzstabilisierungsgesetz)

Prior to AMNOG instatement in January 2011(2), Germany remained one of the few Western countries to allow free drug pricing, which resulted in higher prices than those seen across the EU on average. With healthcare costs skyrocketing, the government introduced AMNOG, or the “Arzneimittelmarktneuordnungsgesetz” (German Medicines Market Reorganization Act), requiring pharmaceutical companies to prove additional benefit over existing treatments and enter into price negotiations for reimbursable medicines after 12 months of free pricing(2).

The implementation of this act brought about negotiated prices that were ~24.5% lower than those at initial launch(3). However, continuing to face both rising drug prices, particularly from high-priced novel oncology agents, and pressure to reduce healthcare costs, the government today is similarly looking to contain costs by implementing reforms to the Statutory Health Insurance System. The reforms, first proposed by Health Minister Professor Karl Lauterbach as part of the draft “Statutory Health Insurance (SHI) Financial Stabilization Bill” (GKV Finanzstabilisierungsgesetz) in March 2022, seek to bridge the €17B short-term deficit facing the statutory health insurance system (SHI)(4). After a quick withdrawal and lengthy discussions, the cabinet passed the bill in July containing several cost-containment measures including:

- Reduction of the free the free pricing period from 12 months down to 6, with the rebate applying from Month 7 following launch;

- Lowered orphan drug threshold for the benefit assessment from €50M to €30M;

- Modifications to rebate negotiations to grant the GKV-SV greater power, whereby medicines offering a “minor” or “unquantifiable additional benefit” will be priced at parity with patent-protected comparators, a “no additional benefit” will generally lead to lower rebated prices than comparators, a “considerable” or “major additional benefit” will be exempt from guidelines, and a discount formula applying to patent-protected comparator therapies that have not had a benefit assessment (e.g., if launched before AMNOG);

- A mandatory 20% rebate for combination products

- Budget and volume agreements to be included in price negotiations that will also apply to follow on indications in the future;

- Penalties for uneconomical pack sizes;

- An extension of the price freeze for another 4 years(1) (introduced in 2010 to allow very limited, “inflation reflecting” reimbursement of price increases for medicines);

- An increase of the mandatory manufacturer discount from 7% to 12% for one year

“The incoming reduced free pricing period will likely disrupt both ‘classic’ launch-sequencing and first-year revenue forecasting in the EU”

Pharmaceutical companies are not the only stakeholders on the lookout for the long-lasting effects these reforms may have; the bill has been met with strong opposition from many organizations. The Federal Council heavily criticized the reforms, noting that, as a share of total SHI expenditure, pharmaceutical spending has remained stable as of late.

Additionally, health and economic committees state that “the planned changes in the AMNOG procedure and the further pharmaceutical price regulations will place a disproportionately heavy burden on pharmaceutical companies, run the risk of preventing (re)establishment of pharmaceutical or active ingredient manufacturers and of making innovation activities more difficult for research-based companies. They are not suitable for strengthening Germany as a pharmaceutical and research location”(5).

The German Association of Research-Based Pharmaceutical Companies (VFA) similarly suggested that the bill will weaken the pharmaceutical presence and healthcare in Germany(5).

Potential Impact of “Financial Stabilization of the Statutory Health Insurance System” (GKV-Finanzstabilisierungsgesetz)

The first ripples from the impact of the new bill are already materialising, with Janssen’s recent postponed DE launch of Tecvayli (teclistamab), a first-in-class bispecific antibody for treating Multiple Myeloma, making the therapy solely available through early access programme. The company cited the AMNOG system as both “outdated” and “anti-innovation” since it will not recognize the clinical phase 1/2 evidence with which the European Commission allowed conditional approval, leaving them to “critically examine the market entry and its possible timing”(6). Janssen alluded to the upcoming AMNOG reforms, saying they hope “the benefit assessment will be open to innovation in the future after the end of the current legislative process”(6). Given the uncertainty surrounding the new bill and its potentially negative effect on innovation, Janssen’s decision may set a precedent for pharmaceutical companies moving forward.

Due to the 12-month free pricing period during which the G-BA currently conducts their benefit assessment, Germany is typically a first-launch market within the EU, especially for oncology treatments and other high-priced medicines. This period of free pricing allows for a high, visible list price across the EU and the world for a year, and the price is used as a reference for other markets during price negotiations. Consequently, not launching in Germany first was almost unfathomable, and Germany has become known for its rapid patient access to innovative treatments; however, this may no longer be the case.

The recent legislation is set to slash the free pricing period in half, and as such, this change has become the most scrutinized aspect of the new reforms. The shortening of the free pricing period was suggested in 2021 by G-BA chair Josef Hecken who noted that the G-BA makes a decision on whether a drug has added benefit in only 6 months, not 12. Thus, AMNOG negotiated prices could retrospectively apply from the time of the decision at Month 7, as opposed to waiting until Month 13(7). Pharma companies have been highly critical of this idea as it may have large knock-on effects across the industry, requiring companies to rethink their German launch strategy.

What will a reduced free pricing period mean for launch sequencing?

Although all elements of the “Statutory Health Insurance (SHI) Financial Stabilization Bill” (GKV Finanzstabilisierungsgesetz) mandate careful consideration, the incoming reduced free pricing period will likely disrupt both ‘classic’ launch-sequencing and first-year revenue forecasting in the EU. In light of this 6-month reduction, pharmaceutical companies need to discuss how to adapt future market access strategies and launch sequence as soon as possible.

How and when manufacturers should engage with country-level payers is becoming increasingly important as these German reforms, and other similar changes across the world, are being instated.

If the lower, negotiated list price becomes visible in half the time, this price is likely to be used in external reference pricing (ERP), and lower prices may be seen across the EU and the rest of the world. This may lead to pharmaceutical companies only seeing half the revenue typically forecasted within Germany in the first year of launch and reduced price in other countries leading to a more significant revenue loss. The revenue loss incurred by pharmaceutical companies is not to be ignored, so while every asset has its own considerations, tailored pricing and market access strategy, it is vital to start considering some more generalized risk mitigation strategies.

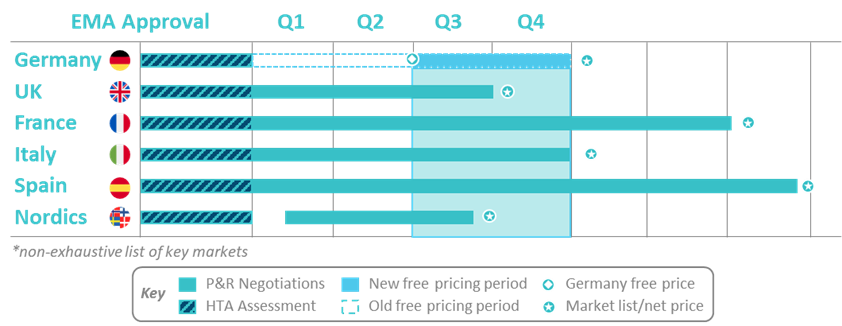

Figure 1: To adapt launch-sequence strategies to the new AMNOG reforms, pharmaceutical companies may instead consider starting negotiations in key EU markets early and therefore subsequently delay launch and the free pricing period in Germany

As one of these mitigation strategies, Pharma companies may decide to postpone the launch in Germany and initiate HTA processes earlier in other EU markets to alleviate external price referencing risk. A 6-month delay would result in the conclusion of pricing negotiations and list price publishing aligning with respect to other HTA timelines across the EU as it typically has in the past (see Fig. 1).

The risks associated with ERP may be partially mitigated with prudent timing, but this does not come without a potential ethical dilemma. By disincentivising earlier launch in Germany with a reduced free pricing period, patient access to novel treatments will be delayed; this, as stakeholders suggest, may even destabilize the country’s status as a front-runner for rapid access and innovation in Europe.

Concluding Remarks

The cost-containment measures associated with the “Statutory Health Insurance (SHI) Financial Stabilization Bill” (GKV Finanzstabilisierungsgesetz), will send a ripple effect through the EU and the rest of the world, but to what extent is currently unclear. Market access strategies and reimbursement preparations will need to be developed as early as possible in order to minimize the potential negative impacts of a truncated free pricing period on global patient access and revenue. This may involve reallocation of resources to mitigate potential revenue losses, with strategies such as increased usage of AI, or increased applications to EUnetHTA to accelerate the HTA process.

While we will have to wait to understand the full impact of the new bill, it is clear that it will be crucial for pharmaceutical companies to be proactive rather than reactive as we navigate through the uncertainty.

Proactive risk mitigation strategies & tactics must be meticulously considered & deployed to optimize outcomes for pharma, healthcare systems, and, most importantly, patients.

Get in touch to find out how we can support you in your European market access, pricing, reimbursement, & launch strategies

References

- https://www.bundesgesundheitsministerium.de/fileadmin/Dateien/3_Downloads/Gesetze_und_Verordnungen/GuV/G/GKV-Finanzstabilisierungsgesetz_Kabinettvorlage.pdf

- https://www.g-ba.de/english/benefitassessment/

- https://www.hbs.edu/faculty/Pages/item.aspx?num=58393

- https://www.thelocal.de/20220628/german-health-insurance-costs-set-to-rise-significantly/

- https://www.vfa.de/de/presse/pressemitteilungen/pm-023-2022-bundesregierung-dreht-innovationen-den-hahn-zu.html#:~:text=Mit%20dem%20Kabinettsbeschluss%20f%C3%BCr%20das,t%C3%A4tigen%20forschenden%20Pharmaunternehmen%20eine%20Z%C3%A4sur.

- https://www.aerztezeitung.de/Wirtschaft/Janssen-fuehrt-neues-Blutkrebsmittel-nicht-in-Deutschland-ein-432063.html

- https://www.aerzteblatt.de/n120632